June 13, 2026 5:18 am

AI Budgeting Tools vs Traditional Budget Spreadsheets: Which Saves More Money?

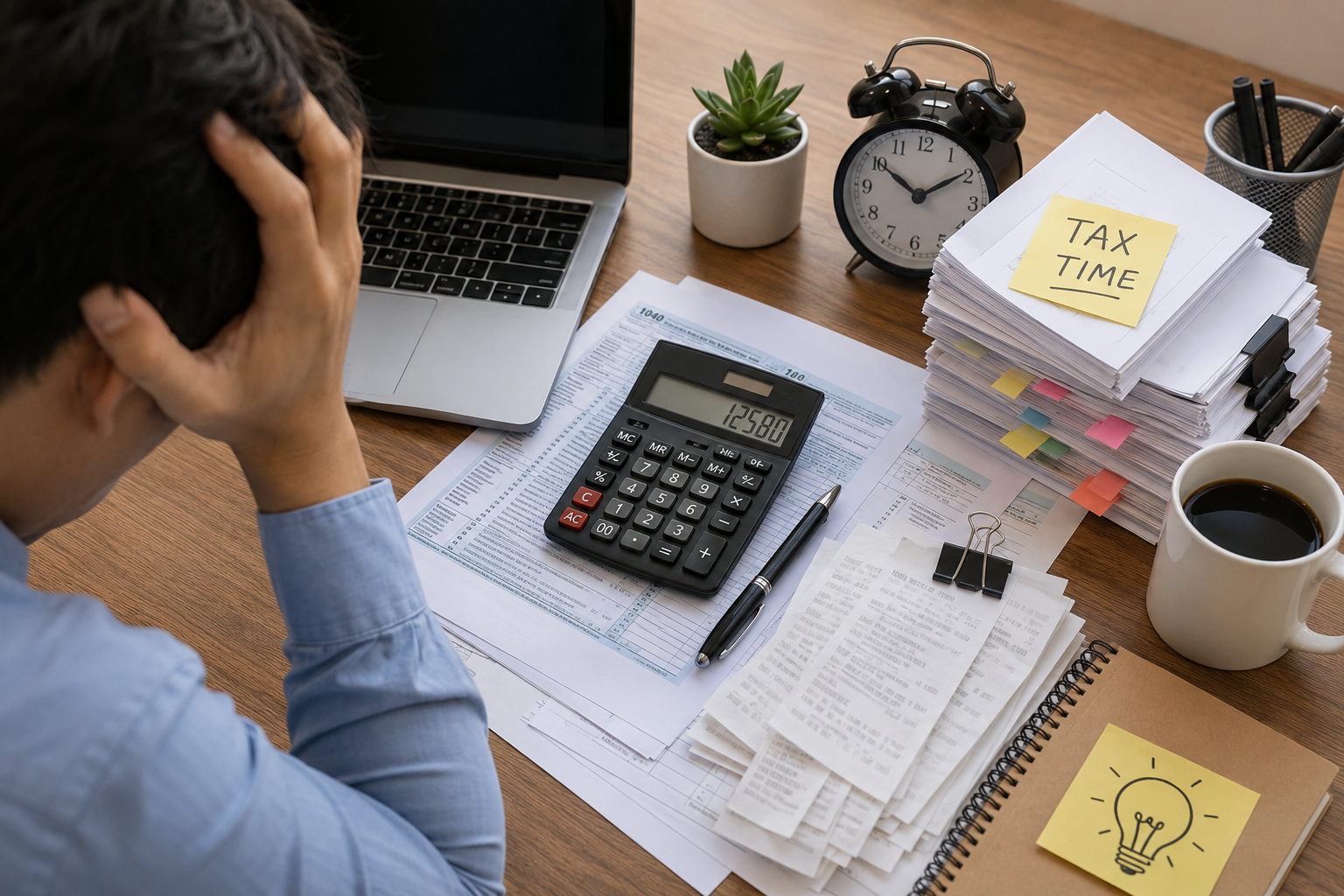

In the debate between AI budgeting tools and traditional spreadsheet budgeting, there is no one-size-fits-all winner — but there is a clear shift in how people manage money in 2026. While spreadsheets offer full control, customization, and privacy, AI budgeting apps deliver automation, real-time insights, and effortless tracking that helps users stay consistent. As financial stress and living costs continue to rise, the real question is no longer which system is more powerful, but which one you will actually stick with long enough to save more money.

- May 29, 2026

- nazneen

- 10:46 pm

- Budgeting & Finance Tips

Two types of people are managing their money better than most right now: those who’ve built disciplined spreadsheet habits, and those who’ve handed the tracking over to an AI-powered app. Everyone in between – intending to budget but not quite doing it consistently – is where most overspending happens.

With living costs higher than they’ve been in years and financial stress affecting more households, the question of how to budget has become as important as whether to budget. AI budgeting tools and traditional spreadsheets represent two genuinely different approaches, each with real strengths. Here’s an honest comparison of both so you can choose what actually fits your life.

What Traditional Spreadsheet Budgeting Actually Is

Spreadsheet budgeting means tracking your income and expenses manually – usually in Excel or Google Sheets – using either a template or a system you’ve built yourself. You enter transactions, categorize spending, and review totals at whatever frequency you choose.

What it does well:

Complete customization is the biggest advantage. You can build a budget that tracks exactly the categories that matter to your life, in exactly the format you find useful. Nothing is automatic – which sounds like a downside but also means nothing is miscategorized by an algorithm that doesn’t understand your spending context.

The manual entry process itself has a psychological benefit many people underestimate. When you type in every transaction, you see your spending in a way that passive automatic tracking doesn’t force. Research consistently shows that manually engaging with financial data increases awareness and tends to reduce discretionary overspending.

Spreadsheets are also free or near-free, private (your data stays on your device), and don’t require linking bank accounts to third-party platforms.

Where it breaks down:

The system only works if you actually do it. Most people start strong and gradually stop entering transactions as life gets busy. A spreadsheet with three weeks of data and a gap is less useful than no budget at all, because it gives false confidence without accurate information.

Manual entry also introduces errors – missed transactions, wrong categories, math mistakes – that compound over time. And for people managing complex finances (multiple income sources, investments, side income), the maintenance burden becomes significant.

What AI Budgeting Tools Actually Do

AI budgeting apps connect to your bank accounts and credit cards, automatically import transactions, categorize spending, and generate insights about your financial habits – often in real time. Examples include Rocket Money, Monarch Money, YNAB, Cleo, and Copilot Money.

What they do well:

Automation is the core value. Your spending is tracked whether or not you remember to open the app. Subscriptions are flagged. Spending patterns are identified. Many apps send alerts when you’re approaching a category limit or when a recurring charge increases.

This consistency is where AI tools genuinely outperform spreadsheets for most users. A budgeting system that runs automatically in the background produces more accurate data than one requiring daily manual effort that many people eventually abandon.

AI tools are also significantly faster to set up for basic budgeting. Linking accounts and reviewing pre-populated categories takes minutes rather than the hours required to build a functional spreadsheet from scratch.

Where they fall short:

Most capable AI budgeting apps carry monthly subscription costs – typically $8 to $15 per month, sometimes more. For someone already struggling with expenses, adding another subscription to manage financial stress is a genuine irony worth noting.

Privacy is a legitimate concern. These apps require access to your bank transaction data. Reputable platforms use bank-level encryption, but connecting financial accounts to third-party software carries inherent risk that spreadsheets don’t.

Automatic categorization also makes mistakes – sometimes persistently. A grocery purchase at a store that also sells clothing might get miscategorized for months before you notice. AI tools require periodic review to stay accurate, just different from the constant review spreadsheets demand.

Discount Calculator

Enter any original price and a discount percentage to instantly see your final price, exact savings, and whether the deal is genuinely worth it.

Side-by-Side: The Honest Comparison

| Feature | AI Budgeting Tools | Traditional Spreadsheets |

|---|---|---|

| Setup time | Fast (minutes) | Moderate (hours) |

| Ongoing effort | Low (automatic) | High (manual entry) |

| Accuracy | High if accounts synced | Depends on user discipline |

| Customization | Medium | High |

| Cost | $8–$15/month typically | Free |

| Privacy | Third-party data access | Fully private |

| Consistency | Automatic | Requires habit |

| Financial awareness | Passive | Active (higher engagement) |

| Best for | Busy users, beginners | Detail-oriented, privacy-focused |

Which One Actually Saves More Money?

The honest answer: the one you use consistently.

An AI app running silently in the background saves more than a spreadsheet that gets abandoned after three weeks. A disciplined spreadsheet user who reviews their finances weekly saves more than someone who downloaded an app, glanced at it twice, and forgot the password.

That said, there are patterns worth noting:

AI tools tend to win on consistency. The barrier to ongoing use is lower – transactions appear automatically, insights surface without effort, and alerts create touchpoints that keep finances visible. For people who’ve tried and failed at manual budgeting, the automation removes the most common failure point.

Spreadsheets tend to win on awareness. The act of manually entering and categorizing expenses creates a level of financial engagement that passive automatic tracking doesn’t replicate. People who maintain spreadsheet budgets often develop a more intuitive sense of their spending patterns over time.

The hybrid approach often produces the best results. Using an AI tool for automatic transaction tracking and a simple spreadsheet for monthly review and planning combines the consistency of automation with the awareness of manual engagement. Many financially organized people use both.

When to Choose Each Option

Choose an AI budgeting app if:

- You’ve tried manual budgeting and stopped within two months

- You have multiple accounts and income sources that are complex to track manually

- You want subscription monitoring and automatic alerts

- Time is your biggest constraint

Choose a spreadsheet if:

- You’re privacy-focused and prefer not to link bank accounts to third-party apps

- You want precise customization the app doesn’t offer

- You have complex financial tracking needs (business income, investments, property)

- The manual engagement helps your financial discipline

Use both if:

- You want automatic tracking with intentional monthly review

- You’re building long-term financial awareness alongside day-to-day convenience

Common Budgeting Mistakes Both Systems Can’t Fix Alone

Neither tool resolves the behavioral side of overspending. The most common budgeting failures aren’t about which software you use:

Saving what’s left over – If savings happen after discretionary spending, they rarely happen. Automate savings at the start of the month regardless of which system you use.

Not reviewing regularly – An AI app generates insights you never read saves nothing. A spreadsheet updated but never analyzed saves nothing. Both systems require periodic intentional review to produce results.

Underestimating subscriptions – The average person significantly underestimates monthly subscription costs. AI tools are particularly good at surfacing these; take the list seriously.

Treating the budget as punishment – Budgets that feel restrictive get abandoned. Build in a realistic wants allocation so the system is sustainable.

Conclusion

AI budgeting tools and traditional spreadsheets are genuinely different tools solving the same problem through opposite approaches. AI wins on automation, consistency, and ease of use. Spreadsheets win on customization, privacy, and active financial engagement.

For most people – especially those who’ve struggled with consistency – an AI tool removes the main barrier to actually tracking spending. For detail-oriented users who want full control, spreadsheets remain excellent. For anyone serious about financial awareness, combining both is worth the extra effort.

The best budgeting system is whichever one you’ll still be using in six months.

Frequently Asked Questions

For consistency and automation, yes. For customization and privacy, spreadsheets have the edge. The better question is which approach matches your habits — a simpler system you use beats a sophisticated one you abandon.

Reputable apps use bank-level encryption and read-only account access (they can see transactions but can’t move money). The risk is real but manageable – stick to established platforms with strong privacy track records and reviews.

AI budgeting apps have a lower barrier to entry and require less setup discipline. For someone new to budgeting, starting with an app and adding spreadsheet habits later as financial awareness grows is a practical approach.

Absolutely. A well-maintained Excel or Google Sheets budget is highly effective. The limitation is the discipline required to maintain it – which is where AI tools have a practical advantage for most users.

How Inflation Is Changing Online Shopping Behavior Worldwide

Popular Right Now

Featured Calculators

Discount Calculator

Enter any original price and a discount percentage to instantly see your final price, exact savings, and whether the deal is genuinely worth it.

Deal Value Checker

Don't just see the % off — get a deal score from 1–10 and a clear verdict: Worth It, Average, or Bad Deal. Stop getting fooled by inflated "original" prices.

About Author

nazneen

Kitchen Chronicles

When it comes to everyday messes, you need a paper towel that’s strong, absorbent, and cost-effective.

Some of Our Top Posts

Populaar Tools

Selected For You

Related Posts

Start Saving Money

in Seconds

Join 10,000+ shoppers using Daily Discount Hub to spend less and live better.

Pick a tool and find out how much you can save right now. Make better spending decisions starting today.