June 13, 2026 4:27 am

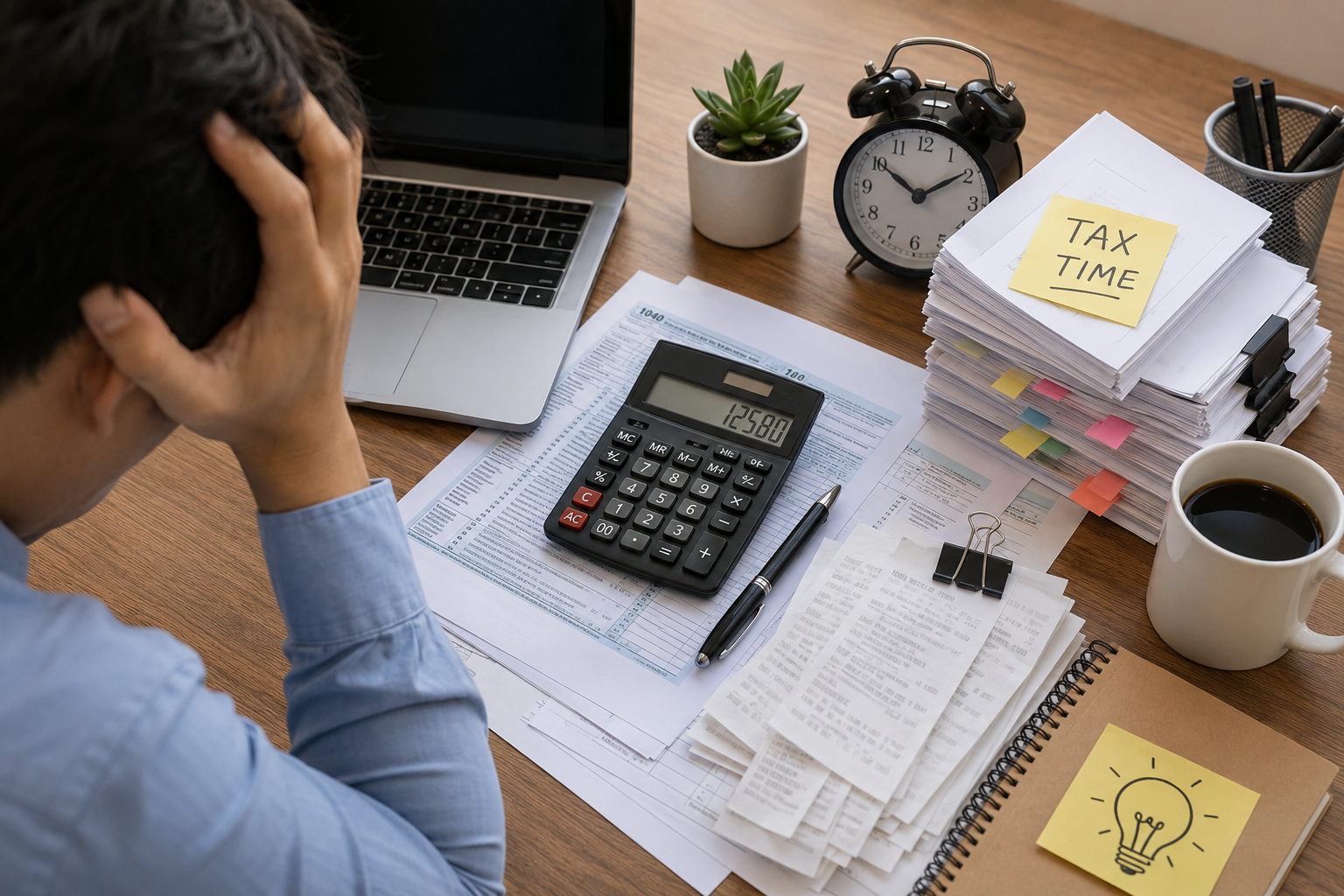

Expense Tracking for Freelancers: Manage Irregular Income & Build Financial Stability

Freelancing comes with freedom - but also financial uncertainty. Without a fixed salary, managing expenses and income becomes a real challenge. This guide breaks down simple, practical methods to track spending, handle irregular income, and build a stable financial system that works even when your earnings fluctuate.

- June 9, 2026

- nazneen

- 11:26 am

- Budgeting & Finance Tips

Freelancing offers remarkable freedom – but that freedom comes with a financial trade-off that most traditional budgeting advice simply isn’t designed to handle. Unlike salaried employees who receive the same deposit on the same date every month, freelancers and gig workers deal with income that arrives in unpredictable bursts. A client pays late. A project falls through. A dry spell hits right when rent is due.

The core challenges are threefold: income inconsistency, delayed client payments, and fluctuating workloads. These three forces combine to make conventional budgeting – “spend less than you earn this month” – nearly meaningless when “what you earn this month” is an unknown variable.

This is precisely why expense tracking for freelancers is not a nice-to-have. It is the foundation of financial survival. When you cannot control when money comes in, the one thing you can control is where it goes out. That control starts with tracking.

Understanding Irregular Income and Its Financial Impact

To manage irregular income effectively, you first need to understand what it actually costs you. The financial impact of income volatility is broader than most freelancers initially realise.

When a high-earning month follows months of quiet, it is tempting to treat the windfall as permission to spend freely – on new equipment, eating out more, upgrading subscriptions. The problem is that next month’s income is not guaranteed to match. Overspending during good months is one of the most common causes of financial stress for freelancers, because the consequences don’t show up immediately. They arrive two or three months later when the pipeline has dried up.

On the other side, slow periods create pressure on fixed obligations: rent, loan repayments, utility bills, and insurance premiums – costs that don’t shrink just because your income did. Without a financial cushion, even a single quiet month can force difficult trade-offs.

Income volatility also complicates tax management. Unlike employees whose taxes are withheld automatically, freelancers must manually set aside money for quarterly or annual tax obligations. An unpredictable income makes this harder to calculate and easier to neglect.

Why Expense Tracking Is Essential for Freelancers

Tracking your expenses doesn’t change what you earn – but it fundamentally changes how far that money goes. Here is why it matters so much for freelance income management:

- It exposes spending leaks. Small recurring costs – streaming services, unused SaaS subscriptions, daily coffee – are invisible until you add them up. Tracking makes them visible.

- It creates predictable patterns. Even with unpredictable income, your expenses tend to be fairly consistent month to month. Knowing your real monthly cost of living is the single most useful number for freelance budgeting.

- It helps you plan for taxes. Once you know what you spend, you can calculate what you genuinely need to earn – and set aside the right percentage for tax before you touch the rest.

- It reduces financial anxiety. Most freelance money stress comes from uncertainty. When you know exactly where every rupee or dollar goes, uncertainty shrinks considerably – even if your income doesn’t change.

💡 Quick insight: Studies consistently show that simply writing down expenses – even without changing behaviour – leads to a reduction in discretionary spending. Awareness alone is a budgeting tool.

Step-by-Step Guide to Tracking Expenses as a Freelancer

The best expense tracking system is the one you will actually use. Complexity is the enemy of consistency. Here is a simple, sustainable approach:

Step 1 – Categorise Your Expenses

Divide all expenses into two buckets:

- Fixed expenses: rent, loan EMIs, insurance premiums, internet- costs that are the same every month regardless of income.

- Variable expenses: groceries, utilities, transport, dining, entertainment – costs that fluctuate and can be adjusted.

Add a third category: business expenses (software subscriptions, equipment, client-related costs). Separating these is important for tax deductions.

Step 2 – Record Spending Daily or Weekly

Pick a recording habit and stick to it. Daily takes 2–3 minutes. Weekly takes 10–15 minutes but has more room for error as receipts get lost. Use whatever format removes friction – a notes app, a simple spreadsheet, or a dedicated expense app.

Step 3 – Review Monthly Summaries

At the end of each month, total up your spending by category. Compare it to your income for that month and to the previous month. Look for: unexpected spikes in variable spending, any fixed cost that has crept up, and the ratio of business to personal expenses.

Step 4 – Adjust Going Forward

The monthly review is where tracking becomes budgeting. Identify one or two categories to reduce next month. This keeps the system from becoming passive data collection and turns it into active financial management.

Track your monthly costs instantly. Use our free Expense Tracker Calculator to categorise your spending and see where your money is going each month.

How to Build a Budget Around Irregular Income

Standard budgeting assumes a fixed monthly income. For freelancers, this approach falls apart immediately. The solution is the baseline income method – a budgeting framework built specifically for income fluctuations.

Calculate Your Baseline Income

Look at the past 6–12 months of earnings. Identify your lowest earning month. That is your baseline – the floor you can plan around with confidence. If your lowest month was Rs 50,000, build your essential budget around that figure, not your average or your best month.

Set Your Minimum Essential Expenses

List every expense that must be paid regardless of income: rent, utilities, groceries, debt repayments, insurance. Add these up. This is your non-negotiable monthly floor. If your baseline income does not cover this number, you need either to increase income, reduce a fixed cost, or build a buffer first.

Allocate Everything Else in Order of Priority

Once essentials are funded, allocate remaining income in this order:

- Tax reserve (20–30% of gross income)

- Emergency buffer top-up (until you reach 2–3 months of expenses)

- Business investment (tools, training, equipment)

- Discretionary spending (entertainment, dining, lifestyle)

Use Percentage-Based Budgeting, Not Fixed Amounts

Instead of “I will spend Rs 8,000 on groceries,” try “I will spend no more than 12% of this month’s income on groceries.” Percentages scale with your income automatically, which makes them far more practical for freelancers than rigid fixed figures.

Discount Calculator

Enter any original price and a discount percentage to instantly see your final price, exact savings, and whether the deal is genuinely worth it.

Best Practices for Managing Cash Flow Fluctuations

Good expense tracking and a solid budget still leave you vulnerable to timing issues – a client paying 45 days late while rent is due in 5 days, for example. Managing cash flow means planning for the timing of money, not just the amount.

- Build a 2–3 month emergency buffer. This is the single most impactful thing a freelancer can do. It means a slow month is an inconvenience, not a crisis. Build it before investing in anything else.

- Separate business and personal accounts. Mixing the two makes it impossible to see your true financial position at a glance. Open a dedicated current account for client payments and business expenses.

- Budget for your lowest expected month, always. Base your lifestyle spending on what you reliably earn in a slow month, not what you hope to earn. Any surplus above that becomes savings or investment.

- Pay yourself a salary. Rather than spending client payments directly, transfer a fixed “salary” from your business account to personal each month. This smooths out income spikes and makes personal budgeting straightforward.

- Follow up on invoices proactively. Late payments are one of the biggest cash flow threats for freelancers. Set calendar reminders to follow up on unpaid invoices before the due date, not after.

⚠️ Common trap: Treating your business account balance as “available to spend” is one of the most common freelancer financial mistakes. Remember that a portion of every payment already belongs to taxes.

Tools and Apps for Freelance Expense Tracking

The right tool removes friction from tracking. Here is a practical overview of the main categories:

| Tool Type | Best For | Examples |

|---|---|---|

| Spreadsheet templates | Full control, custom categories | Google Sheets, Excel |

| Mobile expense apps | On-the-go receipt capture | Expensify, Zoho Expense |

| Invoicing + accounting | Combining billing with tracking | Wave, FreshBooks, QuickBooks |

| Budgeting apps | Overall financial overview | YNAB, Mint, Wallet |

| Free online calculators | Quick monthly summaries | Daily Discount Hub Expense Tracker |

For most solo freelancers starting out, a well-structured Google Sheet paired with a free online expense tracker provides everything needed – without subscription costs eating into your margin. As your freelance business grows, accounting software that can handle invoicing, tax estimates, and automatic categorisation becomes worth the investment.

Common Mistakes Freelancers Make With Money Management

Recognising these patterns is the first step to avoiding them:

- Treating high-income months as the new normal. A strong month feels like a trend. It rarely is. Lifestyle decisions made in a good month create fixed costs that survive into slow months.

- Ignoring tax obligations until year end. Self-employed tax bills are often the largest single bill a freelancer faces. Not setting aside a portion of every payment turns a manageable obligation into a crisis.

- Overlooking small recurring expenses. Rs 500 here, Rs 800 there – micro-subscriptions and small daily habits are invisible individually but often total Rs 5,000–10,000 per month when tracked properly.

- Mixing personal and business finances. Without separation, you can’t accurately calculate your real business profit, claim legitimate deductions, or understand your personal cost of living.

- No financial forecasting. Knowing what you earned last month is useful. Knowing what you’re likely to earn next month – based on current client pipeline – is far more useful. Even a rough monthly projection changes how you manage current spending.

How to Build Long-Term Financial Stability as a Freelancer

Expense tracking and budgeting are the foundations, but lasting financial stability as a freelancer requires an additional layer: intentional income architecture.

Pay Yourself a Consistent Monthly Amount

Once your emergency buffer is in place, decide on a reasonable monthly “salary” to transfer to your personal account – an amount your worst recent months could sustain. Keep any excess in your business account as a runway fund. This approach makes personal budgeting as predictable as a salaried job.

Set Income Goals Rather Than Just Reacting to Income

Most freelancers manage money reactively: they earn whatever work comes in and adjust spending accordingly. A more stable approach is to set a minimum monthly income target, track progress weekly, and actively pursue additional work if the month looks short. Goal-setting changes your financial relationship from passive to active.

Diversify Your Client Base

Over-reliance on one or two clients is one of the biggest financial risks a freelancer faces. If your top client represents more than 50% of your income, losing them would be devastating. Actively broadening your client base reduces this single-point-of-failure risk.

Build Passive or Recurring Revenue

Retainer contracts, digital product sales, affiliate income, and content monetisation all provide more predictable monthly revenue than project-based work. Even a small stream of recurring income – Rs 10,000-15,000 per month – significantly reduces the stress of client income fluctuations.

Conclusion – Turning Unstable Income Into Financial Control

Irregular income is not a problem that disappears as you become more successful as a freelancer – it is simply a feature of the work. The freelancers who thrive financially are not the ones who earn the most; they are the ones who have built systems that make unpredictable income manageable.

Expense tracking is the cornerstone of that system. When you know exactly what you spend, you know what you need to earn. When you know what you need to earn, you can plan, save, and invest with confidence — regardless of what this month’s invoices look like.

Start simple: track every expense this month, review it, and identify one area to improve next month. That single habit, compounded over time, is the difference between financial stress and financial stability.

Frequently Asked Questions

Cash flow management is critical for freelancers because income arrives unpredictably – sometimes in large chunks, sometimes not at all. Without actively managing cash flow, it is easy to overspend during good months and struggle to cover rent or bills during slow ones. Good cash flow management ensures essential expenses are always funded regardless of income timing.

Freelancers manage irregular income by tracking all expenses consistently, setting a baseline budget based on their lowest average monthly income, and saving aggressively during high-earning months to cover slow periods. Building a 2–3 month emergency buffer is one of the most effective ways to stay financially stable without needing a fixed salary.

Commonly used tools include Google Sheets or Excel templates for manual tracking, mobile expense apps for on-the-go recording, invoicing platforms that double as expense trackers, and basic accounting software for automated categorisation. Free tools like Google Sheets paired with a simple budgeting template – or an online expense tracker – are often sufficient for solo freelancers starting out.

Freelancers should ideally set aside 20–30% of gross income for taxes and an additional 10–20% as a personal savings buffer. The exact percentage depends on income stability, local tax obligations, and monthly essential expenses. Starting with any consistent saving habit – even 10% – is better than waiting for a “perfect” income month to begin.

Our Process

How it Works

Three steps to an honest deal verdict.

How Inflation Is Changing Online Shopping Behavior Worldwide

Popular Right Now

Featured Calculators

Discount Calculator

Enter any original price and a discount percentage to instantly see your final price, exact savings, and whether the deal is genuinely worth it.

Deal Value Checker

Don't just see the % off — get a deal score from 1–10 and a clear verdict: Worth It, Average, or Bad Deal. Stop getting fooled by inflated "original" prices.

About Author

nazneen

Kitchen Chronicles

When it comes to everyday messes, you need a paper towel that’s strong, absorbent, and cost-effective.

Some of Our Top Posts

Populaar Tools

Selected For You

Related Posts

Start Saving Money

in Seconds

Join 10,000+ shoppers using Daily Discount Hub to spend less and live better.

Pick a tool and find out how much you can save right now. Make better spending decisions starting today.