June 13, 2026 4:35 am

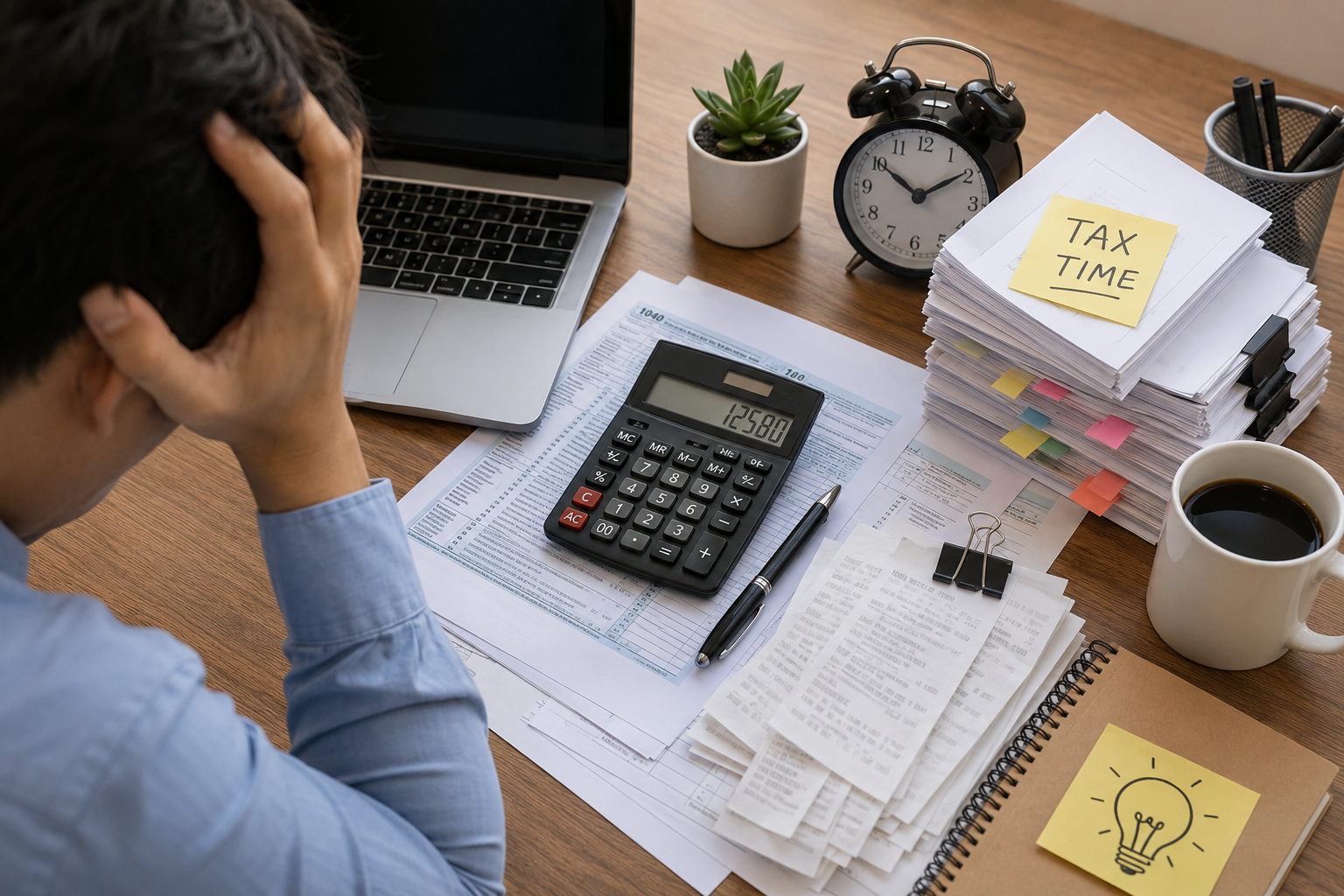

Common Tax Mistakes That Cost You Money (And How a Tax Calculator Prevents Them)

Every year, taxpayers lose thousands due to preventable tax mistakes—missing deductions, choosing the wrong tax regime, underreporting income, overlooking tax credits, or rushing their filing at the last minute. While these errors may seem minor, they can lead to higher tax bills, reduced refunds, penalties, and long-term financial losses. This guide explores the most common tax mistakes made by salaried employees, freelancers, and small business owners, and explains how a tax calculator can help identify deductions, compare tax regimes, estimate liabilities, and improve filing accuracy. Learn how to reduce errors, maximize savings, and file with confidence.This guide explains how deductions, exemptions, and credits can significantly lower your taxable income and overall tax burden. It also highlights how a tax calculator becomes a powerful planning tool, helping you compare scenarios, identify hidden savings, and make informed investment decisions before filing your return. By combining smart deduction strategies with real-time calculations, you can ensure you only pay what is truly required - and not a rupee more.

Every year, millions of taxpayers pay more than they legally owe – not because the tax rates are too high, but because of entirely preventable mistakes. A wrong assumption about deductions. A missed credit. A last-minute filing under pressure. Income from a side project that was never reported. These aren’t rare events – they’re the norm for anyone who approaches taxes reactively instead of proactively.

The frustrating part is that most of these mistakes don’t feel like mistakes when they happen. Choosing the wrong tax regime feels like a neutral default. Not claiming a home office deduction feels like playing it safe. Waiting until March to think about taxes feels like everyone does it.

But the financial consequences are real: higher tax bills, smaller refunds, unnecessary penalties, and missed savings that compound over years. A tax calculator doesn’t eliminate the need to understand your taxes – but it eliminates most of the errors that stem from manual calculation, missed deductions, and poor planning timing.

This guide walks through the most costly tax mistakes taxpayers make – salaried employees, freelancers, and small business owners alike – and shows exactly how catching them early changes your financial outcome.

Why Tax Mistakes Are More Expensive Than Most People Realize

The Hidden Cost of Filing Errors

The most insidious thing about tax mistakes is that many of them are invisible – you never receive a bill for what you could have saved. If you missed a ₹50,000 deduction at a 30% tax slab, you paid ₹15,000 more than you needed to. You’ll never receive a notice about it. The money just quietly leaves your pocket every year.

Lost Refund Opportunities

Many taxpayers are entitled to refunds they never claim – because they filed without accounting for excess TDS deducted by their employer, advance tax already paid, or deductions not declared at the time of investment. A tax calculator run before filing shows your actual liability versus what’s already been paid, surfacing refund opportunities that would otherwise go unclaimed.

Penalties and Interest Charges

On the other side, underreporting income – even accidentally – can trigger demand notices, interest under Sections 234A, 234B, and 234C (in India), and scrutiny assessments. In the US, the IRS charges penalties for underpayment of estimated taxes and late filing. These costs compound over time and are entirely avoidable with accurate, timely calculation.

Long-Term Financial Impact

A taxpayer who overpays by ₹20,000 per year for 20 years – money that could have been invested – loses not just ₹4,00,000 in direct overpayments but potentially ₹10,00,000+ in lost compounding returns. Tax mistakes aren’t one-time events; they’re annual habits with long-term financial consequences.

The Most Common Tax Mistakes That Cost Taxpayers Money

Before diving into each mistake individually, here’s the full list of what consistently costs taxpayers the most:

Choosing the wrong tax regime or misunderstanding marginal rates – paying at a higher effective rate than necessary due to incorrect assumptions about how progressive taxation works.

Missing eligible deductions – failing to claim business expenses, insurance premiums, home loan interest, education loan interest, or charitable donations that are fully within legal entitlement.

Misreporting income – forgetting freelance payments, interest income, capital gains, rental income, or income from part-time work, leading to either underpayment (with penalties) or overpayment (from over-cautious estimation).

Ignoring side hustle and gig income – treating informal or digital income as untaxable, which creates compliance risk and missed deduction opportunities simultaneously.

Waiting until deadline – filing under time pressure leads to missed entries, unchecked figures, and no time to optimize.

Not estimating tax liability before filing – going in blind and discovering an unexpected tax demand or missed refund only after submission.

Overlooking tax credits – confusing credits with deductions or simply not knowing they exist, resulting in paying tax that a credit would have directly eliminated.

Relying on manual calculations – spreadsheet errors, formula mistakes, and outdated rate tables that produce incorrect figures with complete confidence.

Mistake 1 – Selecting the Wrong Tax Regime or Misunderstanding Tax Slabs

How Tax Slabs Work

India’s income tax system is progressive – meaning different portions of your income are taxed at different rates, not your entire income at the highest rate that applies to you. Under the new tax regime for FY 2024–25, income up to ₹3,00,000 is tax-free; ₹3,00,001-₹7,00,000 is taxed at 5%; ₹7,00,001-₹10,00,000 at 10%; ₹10,00,001-₹12,00,000 at 15%; ₹12,00,001-₹15,00,000 at 20%; and above ₹15,00,000 at 30%.

Crucially, if your income is ₹15,50,000, you are not taxed at 30% on the full amount – only the ₹50,000 above ₹15,00,000 is taxed at 30%. Everything below that threshold is taxed at the lower slab rates.

Why Taxpayers Misunderstand Marginal Rates

A very common mistake is believing that crossing into a higher tax slab means the entire income is taxed at the new rate. This causes two problems: taxpayers sometimes deliberately avoid income or investments that would “push them into the 30% bracket,” not realizing they’d only pay 30% on the incremental amount – and they may avoid the old regime when it would actually save them more, given their deduction profile.

Real Example of Overpaying Due to Wrong Regime Selection

Consider a salaried individual with a gross income of ₹14,00,000, paying ₹1,50,000 in 80C investments, ₹25,000 in health insurance premiums (80D), and ₹1,80,000 in home loan interest (Section 24).

Under the old regime: Taxable income = ₹14,00,000 − ₹1,50,000 − ₹25,000 − ₹1,80,000 − ₹50,000 (standard deduction) = ₹10,05,000 → approximate tax liability: ₹1,17,000.

Under the new regime: No deductions apply. Taxable income = ₹14,00,000 − ₹75,000 (standard deduction) = ₹13,25,000 → approximate tax liability: ₹1,50,000+.

Choosing the new regime here without comparing costs this taxpayer over ₹33,000 – every year.

How a Tax Calculator Identifies the Correct Regime

A tax calculator runs both scenarios simultaneously. Enter your income and deductions once; it shows you the liability under both the old and new regime side by side. This comparison, which used to require a spreadsheet and an hour, takes under 60 seconds – and ensures you never pay more than you need to.

Mistake 2 – Forgetting Valuable Tax Deductions

What Tax Deductions Actually Do

Deductions reduce your taxable income – the base on which tax is calculated. Every eligible deduction you claim directly reduces the amount subject to tax. At a 30% slab, a ₹1,00,000 deduction saves ₹30,000 in tax. The higher your income, the more valuable each deduction becomes.

Commonly Missed Deductions

Section 80C (up to ₹1,50,000): EPF, PPF, ELSS mutual funds, life insurance premiums, NSC, 5-year tax-saving FDs, tuition fees for children. Many taxpayers count only their EPF and miss the rest of the ₹1,50,000 ceiling.

Section 80D (up to ₹25,000–₹50,000): Health insurance premiums for self, spouse, children, and parents. The limit increases to ₹50,000 if parents are senior citizens. Widely underused, especially by younger earners who assume they don’t need it.

Section 24(b) – Home Loan Interest (up to ₹2,00,000): The interest component of home loan EMIs is deductible on self-occupied property. Combined with principal repayment under 80C, a home loan is one of the most tax-efficient financial instruments available.

Section 80E – Education Loan Interest: No upper limit. Full deduction on interest paid for higher education loans taken for self, spouse, or children. One of the few uncapped deductions in the tax code – and one of the least claimed.

Section 80G – Charitable Donations: 50%-100% deduction on donations to approved charitable organizations. Keep your receipt and verify the organization’s 80G certification.

Section 80CCD(1B) – NPS Additional Contribution: An extra ₹50,000 deduction over and above the 80C ceiling, exclusively for NPS contributions. At the 30% slab, this saves an additional ₹15,000 – completely separate from the 80C limit.

Employee Deduction Opportunities

Salaried employees often leave money on the table because they declare investments only when HR asks – usually in January or February – and miss anything not on the standard declaration form. House Rent Allowance (HRA) calculation, Leave Travel Allowance (LTA), and professional tax paid are all deductible and are frequently underclaimed or miscalculated.

Self-Employed Deduction Opportunities

For self-employed professionals and business owners under the old regime: office rent, internet and phone expenses, professional software subscriptions, travel for business purposes, depreciation on equipment, and professional development costs are all legitimate deductible expenses. Many self-employed individuals claim only the most obvious deductions and undercount the rest.

Mistake 3 – Underreporting or Overreporting Income

Why Income Reporting Matters

Your tax liability is calculated on your total income from all sources – not just your salary. Every source of income is either taxable, partially exempt, or fully exempt, and each must be correctly categorized and reported. Errors in either direction create problems: underreporting triggers scrutiny and penalties; overreporting means overpaying.

Common Sources of Forgotten Income

Savings account interest: Taxable under “Income from Other Sources.” Many taxpayers assume bank interest is automatically accounted for in Form 16 – it isn’t, unless it was specifically declared.

Fixed deposit interest: Fully taxable. Even if TDS was deducted by the bank, the gross interest must be reported and the TDS credit claimed. Failing to report it while also not claiming the TDS credit means double loss.

Freelance and consultancy payments: Any professional income received – whether through invoices, bank transfers, or UPI – is taxable. The informal nature of many freelance payments creates a false sense that they don’t need to be declared.

Capital gains from mutual funds or stocks: Short-term and long-term capital gains have different tax treatments. Many investors forget to report gains from redeemed SIPs, sold equity shares, or switched mutual fund schemes.

Rental income: Taxable after a 30% standard deduction for repairs and municipal tax paid. Landlords who receive rent informally and don’t receive Form 16 from an employer often omit this entirely.

Risks of Incorrect Reporting

The Income Tax Department’s Annual Information Statement (AIS) aggregates financial data from banks, mutual funds, employers, and property registrars. Discrepancies between your return and your AIS trigger automatic notices. The risk of detection is significantly higher than it was five years ago.

How Tax Calculators Improve Accuracy

A comprehensive tax calculator prompts you to enter income from each category separately – salary, business income, capital gains, other sources – ensuring nothing is overlooked. The structured input process is itself a checklist that reduces omission errors.

Mistake 4 – Ignoring Side Hustle and Freelance Income

Growth of Gig Economy Tax Challenges

Whether it’s freelance design work, YouTube ad revenue, tutoring, food delivery, or selling products online – any income earned beyond a formal salary is taxable. The gig economy has created millions of additional income earners who have no employer managing their TDS and no structured payslip – and who often have no clear idea what they owe or when.

Tax Responsibilities for Freelancers

Freelancers with income above ₹2,50,000 (old regime basic exemption) or ₹3,00,000 (new regime) are required to file returns. If total tax liability exceeds ₹10,000 in a year, advance tax must be paid in quarterly installments (June, September, December, March). Missing advance tax payments triggers interest under Section 234C regardless of whether the final tax is paid on time.

Tracking Additional Income Sources

The practical challenge for gig workers is aggregation – income arrives through multiple channels (bank transfers, PayPal, Razorpay, UPI, cash) without a single consolidated statement. A dedicated income tracker or even a simple running spreadsheet updated monthly prevents the year-end scramble of reconstructing what you earned.

Tax Calculator Benefits for Multiple Income Streams

A tax calculator that accepts income from multiple sources – salary, freelance, rental, capital gains – calculates the aggregate tax liability correctly, accounting for the different treatment of each income type. This is particularly valuable for individuals with both salaried and freelance income, where TDS from the employer may create a false sense that tax obligations are fully covered.

Mistake 5 – Waiting Until the Last Minute

The Cost of Rushed Tax Filing

Filing taxes under a deadline creates a specific type of error: the omission error. When you’re rushing through a return in the final days before July 31st, you skip sections, accept auto-populated figures without reviewing them, and don’t have time to check whether every deduction has been claimed. The cost of this rush isn’t usually a wrong figure – it’s a missing figure.

Common Errors Made Under Pressure

Last-minute filers are significantly more likely to: accept the pre-filled AIS without verifying it, miss deductions not visible in Form 16, forget to claim exempt allowances correctly, enter the wrong bank account for refund, and miss the deadline entirely – triggering late filing fees under Section 234F.

Benefits of Year-Round Tax Planning

The single most impactful habit change in personal tax management is shifting the review from annual to quarterly. A 30-minute review each quarter – checking income received, TDS deducted, investments made, and projected year-end liability – means you arrive at filing time with everything already organized and no surprises.

Using a Calculator for Early Tax Estimates

Running a preliminary tax calculation in April or May – using estimated annual figures – gives you a reliable projection of your tax liability 10–11 months before filing. This projection lets you make investment decisions, plan deductions, and adjust advance tax payments while there’s still time to act.

Mistake 6 – Not Estimating Taxes Before Filing

Why Tax Surprises Happen

A tax demand notice after filing – telling you that you owe ₹40,000 in additional tax – is almost always the result of not having run the numbers before submitting. Most taxpayers assume their employer’s TDS has covered everything. It often hasn’t, because TDS doesn’t account for income from other sources, capital gains, or deductions you didn’t declare to HR.

Understanding Tax Liability in Advance

Your final tax liability is the sum of tax on all income, less all applicable deductions, less all tax credits, less TDS already deducted. If TDS exceeds this final liability, you get a refund. If it falls short, you owe the difference – plus interest if the shortfall exceeded ₹10,000 and advance tax wasn’t paid. None of this should be a surprise at filing time.

Forecasting Refunds and Payments

A pre-filing tax estimate takes 10 minutes with a calculator and tells you exactly what to expect: your final liability, the TDS already paid, and whether you’ll receive a refund or owe additional tax. This forecast allows you to set aside the right amount, file confidently, and avoid both the anxiety of an unexpected demand and the disappointment of an unclaimed refund.

The Role of Tax Calculators in Financial Planning

Beyond filing, regular tax estimates inform better financial decisions throughout the year: whether to make an additional NPS contribution before March 31st, whether a capital gain should be booked now or deferred to the next financial year, whether switching tax regimes next year would save money given a projected income change.

Mistake 7 – Overlooking Tax Credits

Difference Between Credits and Deductions

This distinction is worth repeating because it’s so consequential. A deduction reduces your taxable income – the base on which tax is calculated. A credit reduces your tax payable directly, rupee for rupee. A ₹10,000 deduction at a 20% slab saves ₹2,000 in tax. A ₹10,000 credit saves ₹10,000 in tax. Credits are significantly more valuable when you qualify.

Commonly Missed Credits

Section 87A Rebate: Taxpayers with net taxable income up to ₹5,00,000 (old regime) or ₹7,00,000 (new regime) are entitled to a full tax rebate under Section 87A – meaning zero tax payable. Many eligible taxpayers don’t claim this because they assume any income above zero attracts tax, or because their tax software doesn’t flag it clearly.

TDS Credit (Form 26AS / AIS): Tax deducted at source by employers, banks, and clients must be claimed against your final liability. Taxpayers who don’t reconcile their TDS credits with Form 26AS before filing may either miss credits they’re entitled to or fail to report discrepancies that trigger notices.

Relief Under Section 89: Salaried employees who received salary arrears in a lump sum can claim relief under Section 89 to reduce the tax burden – by calculating tax as if the arrears were received in the year they were due rather than the year they were paid. This is frequently missed because it requires filing Form 10E before submission.

Calculator-Assisted Tax Optimization

A good tax calculator flags applicable credits based on your input – income level, TDS already deducted, regime chosen – and includes them in the final liability calculation. This automated identification catches credits that manual preparation often misses.

Mistake 8 – Manual Tax Calculations

Spreadsheet Errors

A spreadsheet used for tax calculation is only as reliable as its formulas – and formulas break. A cell reference that picks up the wrong row. A formula that doesn’t update when a new deduction is added. A percentage applied to the wrong base. These errors are invisible in the output but produce incorrect tax figures with complete apparent confidence.

Mathematical Mistakes

Even without spreadsheet errors, manual percentage calculations on progressive tax slabs are error-prone. Applying 20% to the wrong income band, forgetting to add cess (4% on income tax), or misapplying the surcharge for higher incomes – each of these produces a different final liability than what you actually owe.

Data Entry Problems

Transcribing figures from Form 16, bank statements, or investment certificates introduces transposition errors – ₹1,24,500 becoming ₹1,42,500, or a ₹50,000 NPS contribution entered as ₹5,000. On individual entries these seem minor; across a full tax calculation they can produce liability differences of tens of thousands.

Why Automation Is More Reliable

A tax calculator applies the correct slab rates, surcharge thresholds, cess percentage, and rebate conditions automatically and consistently – regardless of how many times you run it or what time of night it is. The calculation is the same every time. That consistency is the entire value proposition.

Discount Calculator

Enter any original price and a discount percentage to instantly see your final price, exact savings, and whether the deal is genuinely worth it.

How a Tax Calculator Helps Prevent Costly Tax Errors

Automatic Tax Slab Identification

Enter your total taxable income and the calculator applies the correct slab rates automatically – no need to look up the current year’s rates, remember where each slab begins and ends, or calculate each band separately. It also handles regime-specific differences without requiring you to maintain separate calculations.

Accurate Income Calculations

By prompting entry of each income source separately – salary, business income, capital gains (short-term and long-term), rental income, other sources – a tax calculator ensures comprehensive income aggregation. It applies the correct tax treatment to each category, which manual calculation frequently gets wrong for mixed-income taxpayers.

Deduction Estimation Support

A structured calculator walks you through available deduction sections, prompting entry of 80C investments, 80D premiums, home loan interest, NPS contributions, and other eligible amounts. This guided approach is itself a deduction checklist – reducing the probability that an eligible deduction goes unclaimed simply because it wasn’t top of mind.

Refund and Liability Forecasting

After calculating gross tax liability, a calculator subtracts TDS already deducted and advance tax already paid to show your net position: expected refund or additional payment due. This forecast can be run months before filing, giving you time to optimize rather than react.

Faster Financial Decision-Making

When you can instantly see the tax impact of any financial decision – an additional NPS contribution, a capital gains realization, a change in HRA structure – you make better-informed decisions. The friction of manual calculation is removed, so financial planning becomes responsive rather than theoretical.

Benefits of Using a Tax Calculator Throughout the Year

Better Budget Planning

Knowing your estimated tax liability in advance – rather than discovering it at filing – allows you to budget for the payment, set aside money monthly, and avoid the cash flow disruption of a large lump-sum payment in July.

Tax Saving Strategy Development

Year-round calculator use lets you model decisions before making them: If I invest ₹1,50,000 in ELSS before March 31st, how much does my tax liability change? If I switch to the new regime next year given my expected income increase, what’s the impact? These aren’t complex calculations – but they require a reliable tool to run quickly.

Improved Cash Flow Management

For freelancers and business owners required to pay advance tax quarterly, a tax calculator helps estimate each installment accurately – preventing both underpayment (with its associated interest) and overpayment (unnecessarily tying up working capital with the government).

Reduced Filing Stress

Taxpayers who have been running estimates throughout the year arrive at filing time with no surprises, organized records, and a clear picture of what to expect. The return becomes a confirmation of known figures rather than a discovery of unknown ones.

Higher Confidence Before Submission

Filing with a calculator-verified figure means you submit with confidence rather than anxiety. You know the number is right. You know the deductions are claimed. You know which regime was optimal. That confidence is worth more than the time it takes to run the calculation.

Tax Mistakes Common Among Small Business Owners

Mixing Personal and Business Expenses

Paying personal expenses from a business account – or business expenses from a personal account – creates accounting confusion, makes legitimate deductions harder to claim, and raises red flags in audits. A dedicated business account with all business transactions running through it is the foundation of clean tax management.

Poor Expense Tracking

Business deductions are only as good as the records supporting them. Receipts thrown away, invoices not requested, cash expenses not logged – each one is a deduction forfeited. A consistent habit of digital receipt capture (even a phone photo of every receipt) eliminates most record-keeping problems.

Missing Business Deductions

Small business owners regularly miss deductions for: depreciation on equipment and vehicles, professional membership fees, insurance premiums for business assets, internet and phone costs for business use, software subscriptions, and travel expenses for client visits. Each of these is a legitimate deduction that reduces taxable profit – and business income is often taxed at the highest slab rates, making every deduction particularly valuable.

Incorrect Estimated Tax Payments

Businesses and self-employed individuals whose tax liability exceeds ₹10,000 must pay advance tax in four installments. Underestimating these installments triggers interest under Section 234C even if the final return shows no additional tax due. Overestimating them locks up working capital unnecessarily. A quarterly tax estimate keeps installments accurate.

Tax Mistakes Common Among Freelancers and Gig Workers

Not Tracking Income Properly

When income arrives through multiple channels without a consolidated statement, it’s easy to lose track. A freelancer who received ₹8,00,000 across 12 clients via 4 different payment platforms may genuinely not know their annual income without a dedicated tracking system. This uncertainty leads to either underreporting (risky) or overestimating and overpaying (wasteful).

Forgetting Quarterly Tax Payments

Salaried employees have TDS managed by their employer. Freelancers don’t. If your annual tax liability is likely to exceed ₹10,000, advance tax installments are required – 15% by June 15th, 45% by September 15th, 75% by December 15th, and 100% by March 15th. Missing these deadlines triggers interest charges regardless of whether the total tax is eventually paid correctly.

Missing Home Office Deductions

Freelancers working from home can deduct a proportionate share of rent, internet, electricity, and other home expenses attributable to the workspace – under income from business/profession. This deduction is frequently missed because it feels informal, but it’s entirely legitimate with reasonable documentation.

Poor Record Keeping

Without an employer generating payslips and Form 16, freelancers must maintain their own records: all invoices raised, all payments received, all expenses incurred and their purpose, all TDS certificates received (Form 16A). These records support both accurate filing and audit defense. A simple folder system – digital or physical – updated monthly is sufficient.

Tax Mistakes Common Among Salaried Employees

Incorrect Withholding Assumptions

Many salaried employees assume their employer’s TDS has fully covered their tax obligation. It has – but only for the income and deductions declared to HR. Income from savings interest, dividends, freelance work, or capital gains is not factored into employer TDS. The result is an unexpected tax demand at filing time.

Ignoring Investment Income

Dividends from stocks and mutual funds are taxable as “Income from Other Sources.” Interest from savings accounts above ₹10,000 (₹50,000 for senior citizens) is taxable under Section 80TTA/80TTB. Short-term capital gains from equity funds are taxed at 20%; long-term gains above ₹1,25,000 at 12.5%. Many salaried investors don’t track or report this income, creating discrepancies with AIS data.

Missing Work-Related Deductions

Salaried employees under the old regime can claim deductions for: professional tax paid (fully deductible), unreimbursed business travel expenses in certain cases, and specific allowances structured into their CTC (conveyance, food, telephone). Many employees never review their salary structure for tax efficiency – a conversation with HR at the start of the year can restructure the same CTC into a more tax-efficient form.

Failure to Review Tax Documents

Form 16 is generated by the employer but should be reviewed by the employee before filing. Errors in Form 16 – wrong PAN, incorrect TDS amounts, missing allowances – are not uncommon and must be corrected before the return is filed. Similarly, Form 26AS and AIS should be downloaded and reviewed to ensure all TDS credits are correctly reflected and no unexpected income has been reported against your PAN.

Tax Filing Checklist Before Submission

Use this checklist before submitting any return to catch the most common errors before they’re locked in:

Verify All Income Sources:

- Salary income matches Form 16 Part B.

- Interest income from all bank accounts has been included.

- Capital gains (short-term and long-term) have been calculated and reported.

- Rental income has been reported with the applicable 30% standard deduction.

- Freelance or business income has been included.

Confirm All Deductions

- Total eligible investments under Section 80C have been calculated (up to ₹1,50,000).

- Health insurance premiums under Section 80D have been claimed for yourself and eligible family members.

- Home loan interest deduction under Section 24(b) has been included.

- Additional NPS contributions under Section 80CCD(1B) have been claimed separately.

- Education loan interest under Section 80E has been included where applicable.

- Eligible charitable donations have been supported with Section 80G certificates.

Review Tax Credits

- Section 87A rebate has been applied if taxable income qualifies under the chosen tax regime.

- TDS credits have been verified against Form 26AS and the Annual Information Statement (AIS).

- Advance tax payments have been reflected correctly.

- Relief under Section 89 has been claimed, if applicable, for salary arrears.

Check Personal and Bank Details

- PAN details are correct and match official records.

- The bank account designated for refunds is pre-validated on the income tax portal.

- Email address and mobile number are current to ensure receipt of important notifications and OTPs.

Final Verification

- Tax liability has been cross-checked using a reliable tax calculator.

- The old and new tax regimes have been compared one final time before filing.

- The correct ITR form has been selected based on income sources and taxpayer category.

- All supporting documents have been reviewed and retained for future reference.

- The return has been thoroughly checked before final submission.

Future Trends in Tax Planning and Tax Technology

AI-Powered Tax Tools

Artificial intelligence is being integrated into tax preparation platforms to automatically classify transactions, identify applicable deductions from spending patterns, flag discrepancies between filed returns and financial data, and suggest optimization strategies. The shift is from tools that calculate what you tell them to tools that surface what you might have missed.

Automated Tax Forecasting

The next generation of personal finance tools will forecast tax liability continuously – updating projections in real time as income is received, investments are made, and expenses are logged. Rather than a once-a-year calculation, tax awareness becomes a live financial metric visible alongside bank balances and investment values.

Real-Time Tax Estimation

India’s e-invoicing mandate, real-time GST reconciliation, and the expanding pre-filled return program are all moving toward a model where much of the tax calculation happens automatically – with taxpayers reviewing and confirming rather than building from scratch. For individuals, the equivalent is a pre-populated return that reflects AIS data, requiring only verification and addition of items the system can’t see.

Smarter Financial Planning Tools

The integration of tax calculators with budgeting tools, investment platforms, and expense trackers will allow users to see the after-tax impact of every financial decision in context – making tax awareness a continuous feature of financial management rather than a once-a-year event.

Final Thoughts

The uncomfortable truth about tax mistakes is that most of them are made in good faith – by people who were doing their best with limited information, limited time, or both. The Indian tax system is genuinely complex. The rules change. The forms are dense. The consequences of errors aren’t always immediate.

But the solution isn’t to become a tax expert. It’s to build a small set of reliable habits: track your income consistently, review your deductions before filing, compare tax regimes with real numbers, and use a calculator to verify your liability before submitting anything.

Tax mistakes aren’t inevitable. They’re the product of reactive, last-minute, manual approaches to something that rewards proactive, continuous, and automated management. The tools exist. The time investment is smaller than most people expect. The financial return – measured in taxes not overpaid, refunds not missed, and penalties not incurred – compounds every year.

Frequently Asked Questions

The most consistently costly mistakes are: missing eligible deductions (80C, 80D, home loan interest), selecting the wrong tax regime without comparing both options, not reporting income from all sources (interest, capital gains, freelance earnings), filing at the last minute under pressure, and relying on manual calculations that contain arithmetic or formula errors. Each of these is preventable with basic planning and a reliable tax calculator.

In a progressive tax system, there’s no single “bracket” that applies to all your income – different portions are taxed at different rates. The mistake most people make isn’t choosing the wrong rate but choosing the wrong regime – old vs. new – without comparing which one produces a lower liability given their specific deduction profile. This comparison is the most valuable thing a tax calculator does in under 60 seconds.

Deductions reduce your taxable income before tax is calculated. Credits reduce your tax payable directly after tax is calculated. The practical difference is significant: a ₹50,000 deduction at a 20% slab reduces your tax by ₹10,000; a ₹50,000 credit reduces your tax by ₹50,000. Credits are considerably more valuable – the Section 87A rebate, for example, eliminates all tax payable for eligible taxpayers.

Investment certificates and receipts (80C instruments, insurance premiums, NPS statements), home loan interest certificates, rent receipts and HRA documentation, Form 16 and Form 16A from all TDS deductors, bank statements showing interest income, capital gains statements from mutual fund platforms and brokerages, business expense receipts and invoices if self-employed, and charitable donation receipts with 80G certification.

How Inflation Is Changing Online Shopping Behavior Worldwide

Popular Right Now

Featured Calculators

Discount Calculator

Enter any original price and a discount percentage to instantly see your final price, exact savings, and whether the deal is genuinely worth it.

Deal Value Checker

Don't just see the % off — get a deal score from 1–10 and a clear verdict: Worth It, Average, or Bad Deal. Stop getting fooled by inflated "original" prices.

About Author

nazneen

Kitchen Chronicles

When it comes to everyday messes, you need a paper towel that’s strong, absorbent, and cost-effective.

Some of Our Top Posts

Populaar Tools

Selected For You

Related Posts

Start Saving Money

in Seconds

Join 10,000+ shoppers using Daily Discount Hub to spend less and live better.

Pick a tool and find out how much you can save right now. Make better spending decisions starting today.