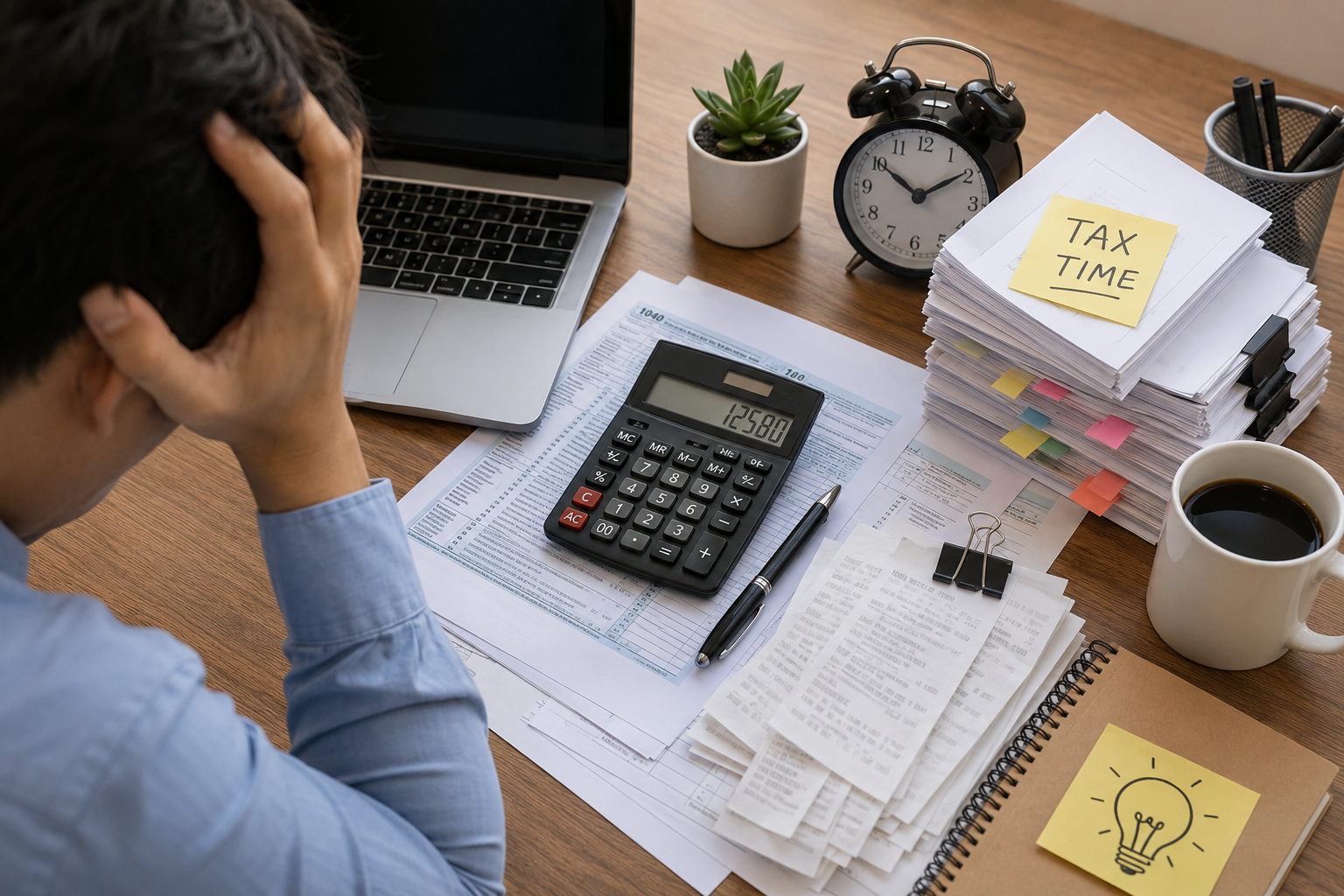

June 13, 2026 4:22 am

How to Reduce Tax Liability Using Smart Deductions (And Why a Tax Calculator Matters)

Tax season often leads to one common problem - people end up paying more than they actually owe. The reason isn’t high tax rates, but missed opportunities like unclaimed deductions, overlooked exemptions, and poor financial planning throughout the year. Reducing your tax liability is not about complex loopholes; it’s about using the benefits already available under tax laws in a smart and structured way.

This guide explains how deductions, exemptions, and credits can significantly lower your taxable income and overall tax burden. It also highlights how a tax calculator becomes a powerful planning tool, helping you compare scenarios, identify hidden savings, and make informed investment decisions before filing your return. By combining smart deduction strategies with real-time calculations, you can ensure you only pay what is truly required - and not a rupee more.

Every year, millions of taxpayers pay more than they legally need to – not because tax rates are unavoidable, but because they miss deductions, overlook exemptions, and file without any real planning. The result is a larger tax bill, a smaller refund, and money left on the table that should have stayed in your pocket.

Reducing your tax liability isn’t about loopholes or complicated schemes. It’s about understanding what the law already allows – and making sure you claim every rupee (or dollar) of it. Combined with a tax calculator, smart deduction planning transforms tax season from a stressful obligation into a genuine financial opportunity.

This guide walks you through everything: what tax liability actually means, which deductions you should never miss, common mistakes that cost people thousands, and how to use a tax calculator to compare scenarios before you file – so you always pay what you owe, and not a rupee more.

Understanding Tax Liability and Why It Matters

Tax liability is simply the total amount of tax you are legally required to pay for a given year. It sounds straightforward – but what most people don’t realize is how many factors influence that number before it’s finalized.

Your tax liability is calculated starting from your gross income: salary, rental income, business earnings, capital gains, and any other taxable source. From that number, eligible deductions and exemptions are subtracted, leaving your taxable income – the figure your tax rate is actually applied to. Depending on which tax slab your taxable income falls under, your base tax is calculated. Then, any applicable tax credits are subtracted directly from that tax amount.

The reason tax liability matters goes beyond just knowing what you owe. Understanding how it’s calculated puts you in control. It means you can make deliberate decisions – about investments, insurance, home loans, retirement contributions – that legally reduce the taxable income number before the slabs are ever applied. That’s where real savings happen.

Most people only think about taxes in March or April. The ones who consistently pay less think about it all year.

Difference Between Deductions, Exemptions, and Tax Credits

These three terms are often used interchangeably – but they work very differently, and confusing them leads to missed savings.

Tax Deductions reduce your taxable income. If your gross income is ₹12,00,000 and you claim ₹1,50,000 in deductions under Section 80C, your taxable income drops to ₹10,50,000. You’re not taxed on that ₹1,50,000 at all. The higher your tax slab, the more valuable each deduction becomes.

Tax Exemptions exclude specific types of income from taxation entirely. House Rent Allowance (HRA), Leave Travel Allowance (LTA), and standard deductions are common examples. The income still exists it simply isn’t counted as taxable. Exemptions are often income-source specific and are claimed before deductions are applied.

Tax Credits are the most powerful of the three because they reduce your actual tax payable – not just your taxable income. If your calculated tax is ₹40,000 and you have a valid tax credit of ₹5,000, you pay ₹35,000. Credits work rupee-for-rupee against your tax bill, making them extremely valuable whenever you qualify.

Understanding which category a benefit falls into helps you prioritize where to focus your planning and ensures you don’t confuse a deduction (partial benefit) with a credit (full benefit).

Most Common Tax Deductions You Should Never Miss

The most expensive tax mistake isn’t filing late or making a calculation error – it’s simply not claiming what you’re already entitled to. Here are the deductions most commonly missed:

Retirement Contributions (Section 80C) Contributions to EPF, PPF, NPS, ELSS mutual funds, and life insurance premiums qualify under Section 80C, with a combined limit of ₹1,50,000 per year. This single section alone can reduce taxable income significantly – yet many salaried individuals only count their EPF and miss the rest.

Health Insurance Premiums (Section 80D) Premiums paid for health insurance – for yourself, your spouse, children, and parents – qualify for deductions under Section 80D. The limit increases further if your parents are senior citizens. This is one of the most under-claimed deductions among younger taxpayers who assume they’re too healthy to bother.

Home Loan Interest (Section 24) If you have a home loan, the interest portion of your EMIs is deductible up to ₹2,00,000 per year on a self-occupied property. Combined with the principal repayment under Section 80C, a home loan can be one of the most tax-efficient financial decisions you make.

Education Loan Interest (Section 80E) Interest paid on loans taken for higher education – for yourself, your spouse, or children – is fully deductible with no upper limit. Most people don’t realize there’s no cap on this one.

Donations to Charitable Organizations (Section 80G) Donations to approved institutions and relief funds qualify for deductions ranging from 50% to 100% of the donated amount. Keep your receipts and check that the organization holds valid 80G certification.

Work-From-Home and Business-Related Expenses If you’re self-employed or a freelancer, expenses directly related to earning income – internet, equipment, office rent, professional subscriptions – are deductible. Salaried employees with unreimbursed work expenses should also review what’s claimable under their tax regime.

Smart Tax-Saving Strategies to Legally Reduce Tax Liability

Knowing what deductions exist is step one. Deploying them strategically throughout the year is step two – and it’s where the real difference in tax bills is made.

Start at the Beginning of the Financial Year, Not the End The single most impactful habit change in tax planning is timing. When you make your tax-saving investments in April instead of February, you gain the benefit all year – whether it’s interest earned in PPF, returns in ELSS, or simply having the money working for you instead of sitting idle until deadline panic sets in.

Invest in Tax-Saving Instruments With Purpose Not all 80C investments are equal. ELSS mutual funds offer market-linked returns with the shortest lock-in (3 years). PPF offers tax-free returns with long-term security. NPS offers an additional deduction of ₹50,000 under Section 80CCD(1B) beyond the 80C limit. Match the instrument to your financial goal, not just your tax-saving target.

Use Income Splitting Where Applicable If you have a spouse or family member in a lower tax bracket, structuring certain investments or income sources in their name can reduce the overall family tax burden. This must be done carefully within legal boundaries- gifts to minors’ income is clubbed with parents’ income, but adult children’s income is not.

Claim Every Eligible Business and Work Expense Freelancers and business owners often undercount deductible expenses out of habit or lack of record-keeping. Software subscriptions, professional development, travel for work, home office utilities – all of these reduce your taxable business income and should be documented and claimed consistently.

Review Your Tax Regime Choice Every Year Under the current dual-regime structure, the optimal choice between the old and new tax regime depends on your specific deduction profile. A tax calculator makes this comparison in seconds. Don’t assume last year’s best choice is still the best choice this year.

How a Tax Calculator Helps You Maximize Savings

A tax calculator is not just a number-checker – it’s a planning instrument. Here’s how it changes the way you approach your taxes:

Instant Liability Estimation Enter your income, and a tax calculator immediately shows your estimated tax under both regimes, with current slabs applied automatically. No manual calculation, no risk of applying the wrong rate. You know your baseline before you’ve made a single planning decision.

Before vs. After Deduction Scenarios This is where a tax calculator earns its value. Enter your income without deductions – see your raw tax. Then add your deductions one by one and watch the number drop in real time. Seeing the exact rupee impact of each deduction turns abstract planning into concrete motivation.

Regime Comparison in Seconds The old vs. new tax regime question used to require a spreadsheet and an hour of calculation. A good tax calculator runs both scenarios simultaneously and tells you precisely which option saves you more based on your individual deduction profile.

Investment Decision Support When you can instantly see that an additional ₹50,000 contribution to NPS reduces your tax by ₹15,000 (at a 30% slab), the investment decision becomes obvious. A calculator makes the tax benefit of every investment tangible before you commit.

Pre-Filing Confidence Using a calculator before filing means you go in knowing your number. You’re not guessing, not relying on an employer’s TDS calculation, and not discovering mid-filing that you missed a deduction category.

Discount Calculator

Enter any original price and a discount percentage to instantly see your final price, exact savings, and whether the deal is genuinely worth it.

Step-by-Step Guide to Using a Tax Calculator Effectively

You don’t need to be a finance professional to use a tax calculator well. Here’s a simple process that takes under 10 minutes:

Step 1 – Enter Your Annual Income Include all sources: gross salary (before any deductions), rental income, freelance or business income, capital gains, and interest income. The more complete your input, the more accurate your estimate.

Step 2 – Add Your Deduction Details Work through each section: 80C investments, 80D premiums, HRA exemption, home loan interest, 80E loan interest, donations, and any other applicable deductions. Use actual figures, not estimates – your bank statements and investment proofs have the exact numbers.

Step 3 – Compare Both Tax Regimes If the calculator offers regime comparison, use it. Input your deductions under the old regime and compare the result against the flat-rate new regime. The right choice is whichever produces the lower tax figure for your specific situation.

Step 4 – Run “What If” Scenarios This is the most underused feature. Ask: What if I invest ₹50,000 more in NPS? What if I increase my 80D premium? What if I prepay part of my home loan? Run each scenario and let the numbers guide your decisions before you make them.

Step 5 – Align Your Investments and Savings Plan Use the output to decide which investments to prioritize before the financial year ends. Set reminders. Make the contributions. Then file with confidence, knowing your tax position has already been optimized.

Common Mistakes That Increase Tax Liability

Most people don’t overpay taxes intentionally – they do it by omission. Here are the most common errors and how to avoid them:

Ignoring Eligible Deductions The most expensive mistake. Many taxpayers claim only 80C (because their employer asks for it) and ignore 80D, 80E, 24(b), and 80G entirely. A quick review of every deduction section before filing can uncover thousands in missed savings.

Not Keeping Financial Records Without receipts, statements, and certificates, deductions can’t be claimed – or may be disallowed during scrutiny. Health insurance premium receipts, donation certificates, home loan interest certificates, and investment proofs should all be organized and filed throughout the year, not hunted down in March.

Filing Without Any Planning Submitting a return based only on Form 16 and salary TDS is the passive approach – and it almost always results in overpayment. Your employer’s TDS calculation doesn’t account for deductions you haven’t declared, investments you made outside salary components, or interest income from other sources.

Choosing the Wrong Tax Regime Without Comparing Defaulting to the new tax regime because “it’s simpler” without actually checking whether your deduction profile makes the old regime more beneficial is a costly assumption. Always compare before choosing.

Waiting Until March to Plan Last-minute investment decisions are made under pressure and often sub-optimal. Locking into a tax-saving FD in February because you ran out of time is worse than a well-chosen ELSS investment made in April of the same year. Plan early; invest deliberately.

Keywords: tax filing mistakes, overpaying taxes, missed deductions, tax planning errors

Advanced Tips to Legally Minimize Taxes

Once the fundamentals are covered, these higher-level strategies can unlock additional savings for those who qualify:

Use the NPS Section 80CCD(1B) Limit Fully NPS contributions up to ₹1,50,000 qualify under 80C – but there’s an additional ₹50,000 deduction available exclusively under Section 80CCD(1B). This is over and above the 80C ceiling and is one of the few ways to exceed the standard limit. At a 30% tax slab, this alone saves ₹15,000.

Harvest Capital Losses Strategically If you hold investments that are currently at a loss, selling them before the financial year ends allows you to set off those losses against capital gains – reducing your capital gains tax liability. This strategy, called tax-loss harvesting, is legal, effective, and underused by individual investors.

Claim HRA Correctly When Paying Rent to Parents If you live in your parents’ home and pay them rent, that rent qualifies for HRA exemption – provided the arrangement is genuine, amounts are reasonable, your parents declare the rental income in their return, and you have a proper rental agreement and payment records. Done correctly, this is entirely legal and can be highly tax-efficient.

Shift to Year-Round Tax Planning The biggest differentiator between people who consistently minimize taxes and those who don’t is timing. Reviewing your tax position quarterly – after each major income event, investment, or life change – means adjustments can be made while there’s still time to act. Annual panic-filing locks in whatever position you’ve drifted into by default.

Consider HUF (Hindu Undivided Family) Structure Where Applicable For eligible families, creating an HUF entity provides a separate PAN and a fresh set of basic exemption limits and deduction ceilings. Income genuinely attributable to the HUF is taxed in the HUF’s hands – potentially at a lower effective rate. This requires proper legal and tax advice to set up correctly.

Why Combining Smart Deductions With a Tax Calculator Is Essential

Deductions are the what of tax saving. A tax calculator is the how much and in which combination.

Knowing that Section 80C allows ₹1,50,000 in deductions is useful information. But knowing that your specific combination of 80C, 80D, HRA, and home loan interest drops your total tax by ₹42,000 – and that the old regime saves you ₹8,000 more than the new one given your exact profile – is actionable intelligence.

That’s the difference a calculator makes. It converts general tax knowledge into personalized financial decisions. It removes guesswork. It shows you precisely where the savings are, in your numbers, before you file.

Used together, smart deductions and a tax calculator create a feedback loop: you identify eligible deductions, the calculator quantifies their impact, and that clarity guides your investment and spending decisions going forward. This is what proactive tax planning looks like in practice – and it’s available to anyone willing to spend 10 minutes before filing season begins.

Final Thoughts

Tax filing doesn’t have to mean overpaying. It doesn’t have to mean last-minute stress, missed deductions, or blind trust in an auto-generated TDS figure.

Every legal deduction you’re entitled to exists because lawmakers decided those financial choices – saving for retirement, protecting your health, repaying a home loan, donating to worthy causes – deserve to be encouraged. Claiming them isn’t aggressive tax planning. It’s the system working exactly as intended.

The shift from reactive filing to proactive planning is simpler than most people expect. Learn your deductions once. Use a tax calculator to quantify them. Make your investment decisions based on data, not guesswork. Start in April, not February.

Do that consistently, and you’ll likely never overpay taxes again.

Frequently Asked Questions

A shipping cost calculator eliminates guesswork by providing accurate delivery cost estimates based on package dimensions, weight, carrier, and destination zone. Without one, businesses frequently underprice products – absorbing shipping losses silently – or overprice and lose customers to competitors who’ve done the maths properly. Used at the pricing stage rather than the checkout stage, it’s the most effective tool for building margin accuracy into your e-commerce business from the start.

At minimum quarterly. Most major carriers – UPS, FedEx, USPS – publish annual general rate increases (GRIs) in January, with fuel surcharge adjustments on a monthly basis. If you’re using a dynamic calculator connected to live carrier APIs, updates happen automatically. If you’re entering rates manually, set a calendar reminder for post-January and each quarter thereafter.

Neither is universally better – it depends on your average order value, product margins, and customer geography. A shipping cost calculator helps you model both scenarios accurately: what free shipping threshold maintains your target margin, versus what transparent shipping charge at checkout preserves the customer relationship without surprising them. Most businesses benefit from a free shipping threshold set using actual calculator data, rather than a round-number guess.

Especially small businesses. Large retailers can absorb shipping losses across high order volumes. Small businesses with tighter margins cannot. A shipping calculator levels the playing field by enabling the same data-driven pricing decisions that large operations make – without requiring a logistics team, enterprise software, or significant investment. The tool is free; the margin protection it provides is significant.

Our Process

How it Works

Three steps to an honest deal verdict.

How Inflation Is Changing Online Shopping Behavior Worldwide

Popular Right Now

Featured Calculators

Discount Calculator

Enter any original price and a discount percentage to instantly see your final price, exact savings, and whether the deal is genuinely worth it.

Deal Value Checker

Don't just see the % off — get a deal score from 1–10 and a clear verdict: Worth It, Average, or Bad Deal. Stop getting fooled by inflated "original" prices.

About Author

nazneen

Kitchen Chronicles

When it comes to everyday messes, you need a paper towel that’s strong, absorbent, and cost-effective.

Some of Our Top Posts

Populaar Tools

Selected For You

Related Posts

Start Saving Money

in Seconds

Join 10,000+ shoppers using Daily Discount Hub to spend less and live better.

Pick a tool and find out how much you can save right now. Make better spending decisions starting today.